The EU Corporate Sustainability Reporting Directive (CSRD) is being introduced over the next few years and includes specific reporting requirements on Diversity, Equity, and Inclusion. The EU CSRD revises and strengthens the existing Non-Financial Reporting Directive (NFRD) by enhancing overall organizational disclosure on policies, risks, and results, making them more comparable, comprehensive, and transparent, especially for investors. The new Directive is more comprehensive and transparent than the existing NFRD and increases the number of organizations subject to reporting regulation from 12,000 to what many estimate to be 50,000 organizations.

The new Directive applies not only to organizations in the European Union (EU) but also to subsidiaries of overseas organizations based in the EU, which must also report their activities’ impact on people and the environment (impact materiality) as well as the sustainability matters that financially impact the organization (financial materiality). It introduces more prescriptive measures, and requires the organization’s DE&I information, along with its future plans to be published, independently verified, and fully accessible to all relevant stakeholders.

The CSRD is considerably more forward-looking than previous EU legislation. Organizations are mandated to publish actions and future targets with accompanying milestones, budgets, and organizational resources earmarked to achieve their DE&I strategy and goals. The decision about exactly which information is to be reported will be based on the results of an organization’s materiality analysis.

The Importance of Preparedness

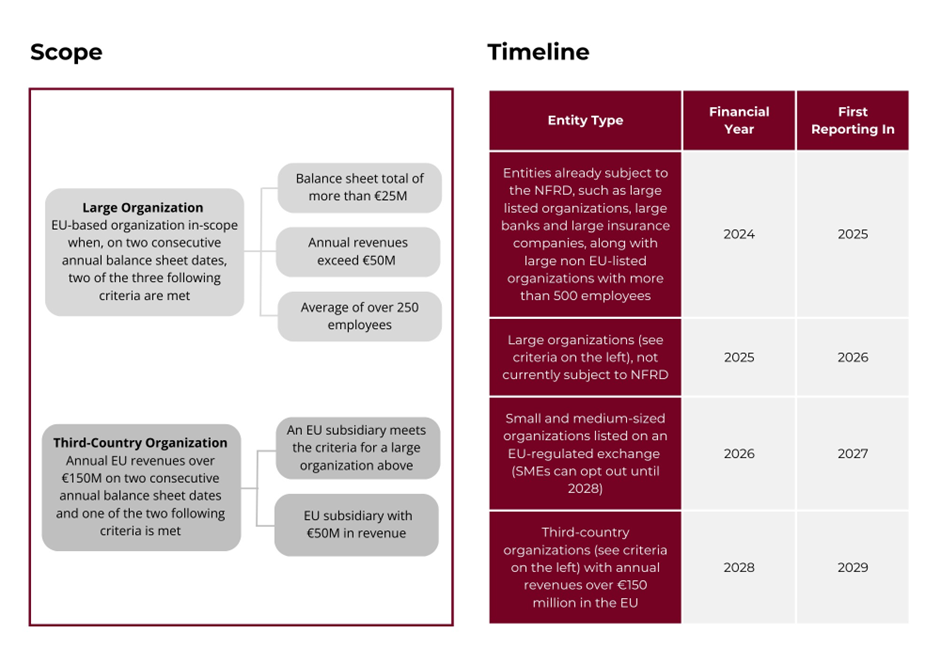

Organizations in scope are strongly encouraged to get prepared in a timely manner for the new reporting requirements which will start applying between 2024 and 2028, depending on the certain characteristics of the organization. The requirements will first extend to large public-interest organizations already subject to the NFRD along with large non-EU listed organizations, followed by other public-interest organizations of a certain size, and finally incorporate listed small and medium-sized entities (see image). Early anticipation and assessment of how an organization will be affected, from when, and which DE&I information is impacted and needs to be reported, will mitigate any risks and provide potential opportunities to streamline disclosure across different reporting and management frameworks.

To comply with the CSRD, organizations are required to use the European Reporting Sustainability Reporting Standards (ESRS) to prepare their ESG disclosure information. The EDGE and EDGEplus Standards are consistent with the vast majority of the content of the ESRS S1 on Own Workforce and can, therefore, provide a strong boost for CSRD compliance in DE&I topics in the workplace. HR and DE&I professionals will be called upon to prepare relevant data and information, whether an organization is reporting on an individual country entity level or consolidated regional or global level.

Clearly Defined DE&I Measures

The EU CSRD’s Standards for DE&I are clearly defined within ESRS S1 Own Workforce, which includes 17 separate measures and requirements ranging from key DE&I policies and practices, targets, and actions, to workforce diversity and pay equity data, almost all of which are easily extractable from information used during the EDGE Certification assessment. This information can be effectively sourced across all three sources of information of the EDGE process, namely statistical data, policies & practices, and employee experience, measured using an employee survey. The latter providing an effective vehicle to drive inclusivity and assess the views, perceptions, and sentiment of the organization’s workforce in a structured manner.

Furthermore, the CSRD requirements open up the assessment of DE&I beyond the gender binary model and towards intersectional equity, thereby supporting a broader DE&I understanding within organizations. EDGE fully supports this direction of travel that mirrors our own developments with the popular uptake of EDGEplus Certification. The requirements within the EU Directive give organizations the opportunity to disclose data and information on managing relevant dimensions of diversity in the workplace including gender identity, age, nationality, working with a disability, sexual orientation, religion/belief, and race/ethnicity, thus deepening the transparency of DE&I related information and addressing equal opportunities afforded to traditionally under-represented groups in the workforce.

Comfort in a Changing Compliance-Driven Environment

We’re witnessing compliance on non-financial topics including DE&I being top of mind for both executives and management teams right now. Effectively navigating an organization’s disclosure requirements across different jurisdictions will prove challenging to monitor and manage. Working with one robust and comprehensive source of holistic DE&I data will support an organization’s ability to report across regulatory frameworks in an effective and consistent manner. Getting external assurance over this information will add to the integrity and credibility of the information, while providing comfort to management on its quality and accuracy, similarly to the independent third-party verification undertaken as part of the EDGE Certification.

Additionally, we expect an increase in the interoperability of the different management and reporting frameworks and standards that will ease the workload on organizations as they seek to comply with current and emerging requirements.

At the same time, perhaps understandably, some organizations continue to lobby for less onerous reporting requirements. Where there is some justification, we have seen small revisions to the draft EU CSRD requirements to lighten the load or postpone the anticipated deadlines for some organizations. But this Directive is EU law. It will be transposed into national law in every Member State. And each state will then decide to enforce this CSRD scope as a minimum standard or choose to enforce a slightly higher standard. For organizations, the sooner they start preparing, the better.